If the thought of investing in the stock market scares you, you are not alone. Individuals with very limited experience in stock investing are either terrified by horror stories of the average investor losing 50% of their portfolio value—for example, in the two bear markets that have already occurred in this millennium—or are beguiled by “hot tips” that bear the promise of huge rewards but seldom pay off. It is not surprising, then, that the pendulum of investment sentiment is said to swing between fear and greed.

The reality is that investing in the stock market carries risk, but when approached in a disciplined manner, it is one of the most efficient ways to build up one’s net worth. While the value of one’s home typically accounts for most of the net worth of the average individual, most of the affluent and very rich generally have the majority of their wealth invested in stocks.1 In order to understand the mechanics of the stock market, let’s begin by delving into the definition of a stock and its different types.

What Is a Stock?

A stock is a financial instrument that represents ownership in a company or corporation and represents a proportionate claim on its assets (what it owns) and earnings (what it generates in profits). Stocks are also called shares or a company’s equity.

Stock ownership implies that the shareholder owns a slice of the company equal to the number of shares held as a proportion of the company’s total outstanding shares. For instance, an individual or entity that owns 100,000 shares of a company with one million outstanding shares would have a 10% ownership stake in it. Most companies have outstanding shares that run into the millions or billions.

Types of Stock

While there are two main types of stock—common and preferred—the term equities is synonymous with common shares, as their combined market value and trading volumes are many magnitudes larger than that of preferred shares.

The main distinction between the two is that common shares usually carry voting rights that enable the common shareholder to have a say in corporate meetings (like the annual general meeting or AGM) where matters such as election to the board of directors or appointment of auditors are voted upon while preferred shares generally do not have voting rights. Preferred shares are so named because preferred shareholders have priority over common shareholders to receive dividends as well as assets in the event of a liquidation.2

Common stock can be further classified in terms of their voting rights. While the basic premise of common shares is that they should have equal voting rights—one vote per share held—some companies have dual or multiple classes of stock with different voting rights attached to each class. In such a dual-class structure, Class A shares, for example, may have 10 votes per share, while the Class B subordinate voting shares may only have one vote per share. Dual- or multiple-class share structures are designed to enable the founders of a company to control its fortunes, strategic direction, and ability to innovate.

Why Companies Issue Shares

Today’s corporate giant likely had its start as a small private entity launched by a visionary founder a few decades ago. Think of Jack Ma incubating Alibaba (BABA) from his apartment in Hangzhou, China, in 1999, or Mark Zuckerberg founding the earliest version of Facebook (now Meta), from his Harvard University dorm room in 2004. Technology giants like these have become among the biggest companies in the world within a couple of decades.

However, growing at such a frenetic pace requires access to a massive amount of capital. In order to make the transition from an idea germinating in an entrepreneur’s brain to an operating company, they need to lease an office or factory, hire employees, buy equipment and raw materials, and put in place a sales and distribution network, among other things. These resources require significant amounts of capital, depending on the scale and scope of the business startup.

Raising Capital

A startup can raise such capital either by selling shares (equity financing) or borrowing money (debt financing). Debt financing can be a problem for a startup because it may have few assets to pledge for a loan—especially in sectors such as technology or biotechnology, where a firm has few tangible assets—plus the interest on the loan would impose a financial burden in the early days, when the company may have no revenues or earnings.

Equity financing, therefore, is the preferred route for most startups that need capital. The entrepreneur may initially source funds from personal savings, as well as friends and family, to get the business off the ground. As the business expands and capital requirements become more substantial, the entrepreneur may turn to angel investors and venture capital firms.

Listing Shares

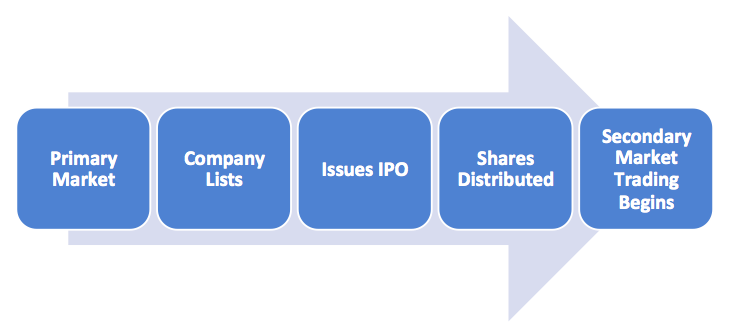

When a company establishes itself, it may need access to much larger amounts of capital than it can get from ongoing operations or a traditional bank loan. It can do so by selling shares to the public through an initial public offering (IPO).

This changes the status of the company from a private firm whose shares are held by a few shareholders to a publicly-traded company whose shares will be held by numerous members of the general public. The IPO also offers early investors in the company an opportunity to cash out part of their stake, often reaping very handsome rewards in the process.

Once the company’s shares are listed on a stock exchange and trading in it commences, the price of these shares fluctuates as investors and traders assess and reassess their intrinsic value. There are many different ratios and metrics that can be used to value stocks, of which the single-most popular measure is probably the price-to-earnings (PE) ratio. The stock analysis also tends to fall into one of two camps—fundamental analysis, or technical analysis.

What Is a Stock Exchange?

Stock exchanges are secondary markets where existing shareholders can transact with potential buyers. It is important to understand that the corporations listed on stock markets do not buy and sell their own shares on a regular basis. Companies may engage in stock buybacks or issue new shares but these are not day-to-day operations and often occur outside of the framework of an exchange.

So when you buy a share of stock on the stock market, you are not buying it from the company, you are buying it from some other existing shareholder. Likewise, when you sell your shares, you do not sell them back to the company—rather you sell them to some other investor.

History of Stock Exchanges

The first stock markets appeared in Europe in the 16th and 17th centuries, mainly in port cities or trading hubs such as Antwerp, Amsterdam, and London.3 These early stock exchanges, however, were more akin to bond exchanges as the small number of companies did not issue equity. In fact, most early corporations were considered semi-public organizations since they had to be chartered by their government in order to conduct business.

In the late 18th century, stock markets began appearing in America, notably the New York Stock Exchange (NYSE), which allowed for equity shares to trade. The honor of the first stock exchange in America goes to the Philadelphia Stock Exchange (PHLX), which still exists today.4 The NYSE was founded in 1792 with the signing of the Buttonwood Agreement by 24 New York City stockbrokers and merchants. Prior to this official incorporation, traders and brokers would meet unofficially under a buttonwood tree on Wall Street to buy and sell shares.5

The advent of modern stock markets ushered in an age of regulation and professionalization that now ensures buyers and sellers of shares can trust that their transactions will go through at fair prices and within a reasonable period of time. Today, there are many stock exchanges in the U.S. and throughout the world, many of which are linked together electronically. This in turn means markets are more efficient and more liquid.

Over-the-Counter Exchanges

There also exists a number of loosely regulated over-the-counter (OTC) exchanges, which may also be referred to as bulletin boards (OTCBB). These shares tend to be riskier since they list companies that fail to meet the more strict listing criteria of bigger exchanges.6 Larger exchanges may require that a company has been in operation for a certain amount of time before being listed and that it meets certain conditions regarding company value and profitability.

In most developed countries, stock exchanges are self-regulatory organizations (SROs), non-governmental organizations that have the power to create and enforce industry regulations and standards.

The priority for stock exchanges is to protect investors through the establishment of rules that promote ethics and equality. Examples of such SRO’s in the U.S. include individual stock exchanges, as well as the National Association of Securities Dealers (NASD) and the Financial Industry Regulatory Authority (FINRA).

How Share Prices Are Set

The prices of shares on a stock market can be set in a number of ways. The most common way is through an auction process where buyers and sellers place bids and offers to buy or sell. A bid is the price at which somebody wishes to buy, and an offer (or ask) is the price at which somebody wishes to sell. When the bid and ask coincide, a trade is made.

The overall market is made up of millions of investors and traders, who may have differing ideas about the value of a specific stock and thus the price at which they are willing to buy or sell it. The thousands of transactions that occur as these investors and traders convert their intentions to actions by buying and/or selling a stock cause minute-by-minute gyrations in it over the course of a trading day.

A stock exchange provides a platform where such trading can be easily conducted by matching buyers and sellers of stocks. For the average person to get access to these exchanges, they would need a stockbroker. This stockbroker acts as the middleman between the buyer and the seller. Getting a stockbroker is most commonly accomplished by creating an account with a well-established retail broker.

Stock Market Supply and Demand

The stock market also offers a fascinating example of the laws of supply and demand at work in real-time. For every stock transaction, there must be a buyer and a seller. Because of the immutable laws of supply and demand, if there are more buyers for a specific stock than there are sellers of it, the stock price will trend up. Conversely, if there are more sellers of the stock than buyers, the price will trend down.

The bid-ask or bid-offer spread (the difference between the bid price for a stock and its ask or offer price) represents the difference between the highest price that a buyer is willing to pay or bid for a stock and the lowest price at which a seller is offering the stock.

A trade transaction occurs either when a buyer accepts the ask price or a seller takes the bid price. If buyers outnumber sellers, they may be willing to raise their bids in order to acquire the stock. Sellers will, therefore, ask higher prices for it, ratcheting the price up. If sellers outnumber buyers, they may be willing to accept lower offers for the stock, while buyers will also lower their bids, effectively forcing the price down.

Matching Buyers to Sellers

Some stock markets rely on professional traders to maintain continuous bids and offers since a motivated buyer or seller may not find each other at any given moment. These are known as specialists or market makers.

A two-sided market consists of the bid and the offer, and the spread is the difference in price between the bid and the offer. The more narrow the price spread and the larger size of the bids and offers (the amount of shares on each side), the greater the liquidity of the stock. Moreover, if there are many buyers and sellers at sequentially higher and lower prices, the market is said to have good depth.

Matching buyers and sellers of stocks on an exchange was initially done manually, but it is now increasingly carried out through computerized trading systems. The manual method of trading was based on a system known as the open outcry system, where traders used verbal and hand signal communications to buy and sell large blocks of stocks in the trading pit or the exchange floor.

However, the open outcry system has been superseded by electronic trading systems at most exchanges. These systems can match buyers and sellers far more efficiently and rapidly than humans can, resulting in significant benefits such as lower trading costs and faster trade execution.

Benefits of Stock Exchange Listing

Until recently, the ultimate goal for an entrepreneur was to get his or her company listed on a reputed stock exchange such as the NYSE or Nasdaq, because of the obvious benefits, which include:

- An exchange listing means ready liquidity for shares held by the company’s shareholders.

- It enables the company to raise additional funds by issuing more shares.

- Having publicly tradable shares makes it easier to set up stock options plans that can attract talented employees.

- Listed companies have greater visibility in the marketplace; analyst coverage and demand from institutional investors can drive up the share price.

- Listed shares can be used as currency by the company to make acquisitions in which part or all of the consideration is paid in stock.

These benefits mean that most large companies are public rather than private. Very large private companies such as food and agriculture giant Cargill, industrial conglomerate Koch Industries, and DIY furniture retailer Ikea are among the world’s most valuable private companies, and they are the exception rather than the norm.

Problems of Stock Exchange Listing

But there are some drawbacks to being listed on a stock exchange, such as:

- Significant costs associated with listing on an exchange, such as listing fees and higher costs associated with compliance and reporting.

- Burdensome regulations, which may constrict a company’s ability to do business.

- The short-term focus of most investors, which forces companies to try and beat their quarterly earnings estimates rather than taking a long-term approach to their corporate strategy.

Many giant startups (also known as unicorns because startups valued at greater than $1 billion used to be exceedingly rare) choose to get listed on an exchange at a much later stage than startups from a decade or two ago.

While this delayed listing may partly be attributable to the drawbacks listed above, the main reason could be that well-managed startups with a compelling business proposition have access to unprecedented amounts of capital from sovereign wealth funds, private equity, and venture capitalists. Such access to seemingly unlimited amounts of capital would make an IPO and exchange listing much less of a pressing issue for a startup.

The number of publicly-traded companies in the U.S. is also shrinking—from more than 8,000 in 1996 to around 4,300 in 2017.78

Investing in Stocks

Numerous studies have shown that, over long periods of time, stocks generate investment returns that are superior to those from every other asset class. Stock returns arise from capital gains and dividends.

A capital gain occurs when you sell a stock at a higher price than the price at which you purchased it. A dividend is the share of profit that a company distributes to its shareholders. Dividends are an important component of stock returns. They have contributed nearly one-third of total equity return since 1956, while capital gains have contributed two-thirds.9

While the allure of buying a stock similar to one of the fabled FAANG quintet—Meta, Apple (AAPL), Amazon (AMZN), Netflix (NFLX), and Google parent Alphabet (GOOGL)—at a very early stage is one of the more tantalizing prospects of stock investing, in reality, such home runs are few and far between.

Investors who want to swing for the fences with the stocks in their portfolios should have a higher tolerance for risk. These investors will be keen to generate most of their returns from capital gains rather than dividends. On the other hand, investors who are conservative and need the income from their portfolios may opt for stocks that have a long history of paying substantial dividends.

Market Cap and Sector

While stocks can be classified in a number of ways, two of the most common are by market capitalization and by sector.

Market cap refers to the total market value of a company’s outstanding shares and is calculated by multiplying these shares by the current market price of one share. While the exact definition may vary depending on the market, large-cap companies are generally regarded as those with a market capitalization of $10 billion or more, while mid-cap companies are those with a market capitalization of between $2 billion and $10 billion, and small-cap companies fall between $300 million and $2 billion.10

The industry standard for stock classification by sector is the Global Industry Classification Standard (GICS), which was developed by MSCI and S&P Dow Jones Indices in 1999 as an efficient tool to capture the breadth, depth, and evolution of industry sectors. GICS is a four-tiered industry classification system that consists of 11 sectors and 24 industry groups. The 11 sectors are:11

- Energy

- Materials

- Industrials

- Consumer Discretionary

- Consumer Staples

- Health Care

- Financials

- Information Technology

- Communication Services

- Utilities

- Real Estate

This sector classification makes it easy for investors to tailor their portfolios according to their risk tolerance and investment preference. For example, conservative investors with income needs may weigh their portfolios toward sectors whose constituent stocks have better price stability and offer attractive dividends through so-called defensive sectors such as consumer staples, health care, and utilities. Aggressive investors may prefer more volatile sectors such as information technology, financials, and energy.

Stock Market Indices

In addition to individual stocks, many investors are concerned with stock indices, which are also called indexes. Indices represent aggregated prices of a number of different stocks, and the movement of an index is the net effect of the movements of each individual component. When people talk about the stock market, they often allude to one of the major indices such as the Dow Jones Industrial Average (DJIA) or the S&P 500.

The DJIA is a price-weighted index of 30 large American corporations. Because of its weighting scheme and the fact that it only consists of 30 stocks (when there are many thousands to choose from), it is not really a good indicator of how the stock market is doing.12 The S&P 500 is a market-cap-weighted index of the 500 largest companies in the U.S. and is a much more valid indicator.13

Indices can be broad such as the Dow Jones or S&P 500, or they can be specific to a certain industry or market sector. Investors can trade indices indirectly via futures markets, or via exchange-traded funds (ETFs), which act just like stocks on stock exchanges.

A market index is a popular measure of stock market performance. Most market indices are market-cap weighted, which means that the weight of each index constituent is proportional to its market capitalization. Keep in mind, though, that a few of them are price-weighted, such as the DJIA. In addition to the DJIA, other widely watched indices in the U.S. and internationally include the:

- S&P 500

- Nasdaq Composite

- Russell Indices (Russell 1000, Russell 2000)

- TSX Composite (Canada)

- FTSE Index (UK)

- Nikkei 225 (Japan)

- Dax Index (Germany)

- CAC 40 Index (France)

- CSI 300 Index (China)

- Sensex (India)

Largest Stock Exchanges

Stock exchanges have been around for more than two centuries. The venerable NYSE traces its roots back to 1792 when two dozen brokers met in Lower Manhattan and signed an agreement to trade securities on commission.5 In 1817, New York stockbrokers operating under the agreement made some key changes and reorganized as the New York Stock and Exchange Board.14

The NYSE and Nasdaq are the two largest exchanges in the world, based on the total market capitalization of all the companies listed on the exchange. The number of U.S. stock exchanges registered with the Securities and Exchange Commission has reached nearly two dozen, though most of these are owned by either CBOE, Nasdaq, or NYSE.15 The table below displays the 20 biggest exchanges globally, ranked by the total market capitalization of their listed companies.

[“source=investopedia”]