Each April, the New York Federal Reserve releases a survey around business owners’ borrowing preferences. Surveys conducted in the past three years point specifically to both the challenges and opportunities community-based lending institutions have in competing with non-chartered online lenders. Below are four key takeaways from the 2019 survey.

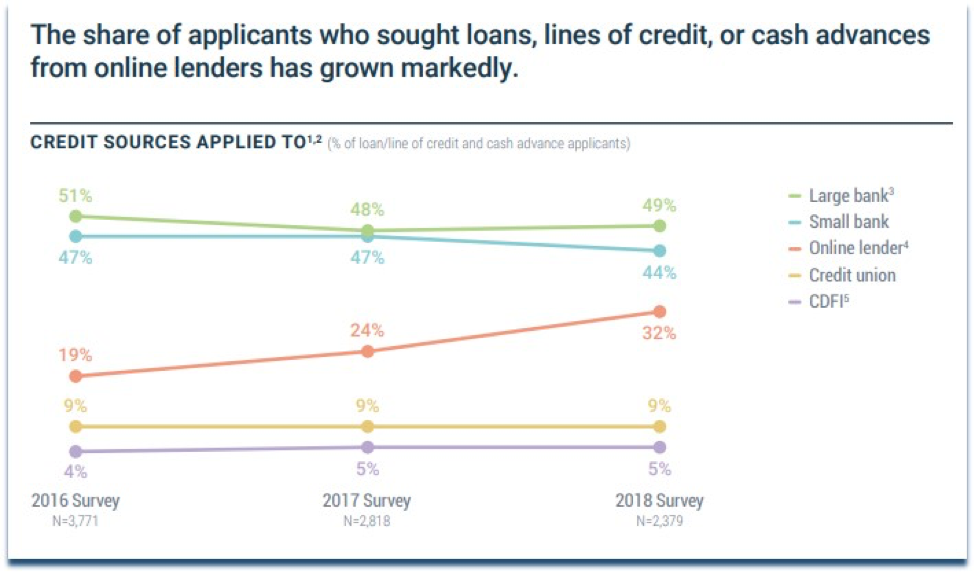

The preference for online origination is growing

Over the past three years, business owners have shown a growing preference toward streamlined loan origination that is initiated online. While banks still maintain a competitive advantage, the trend is clear for online lenders.

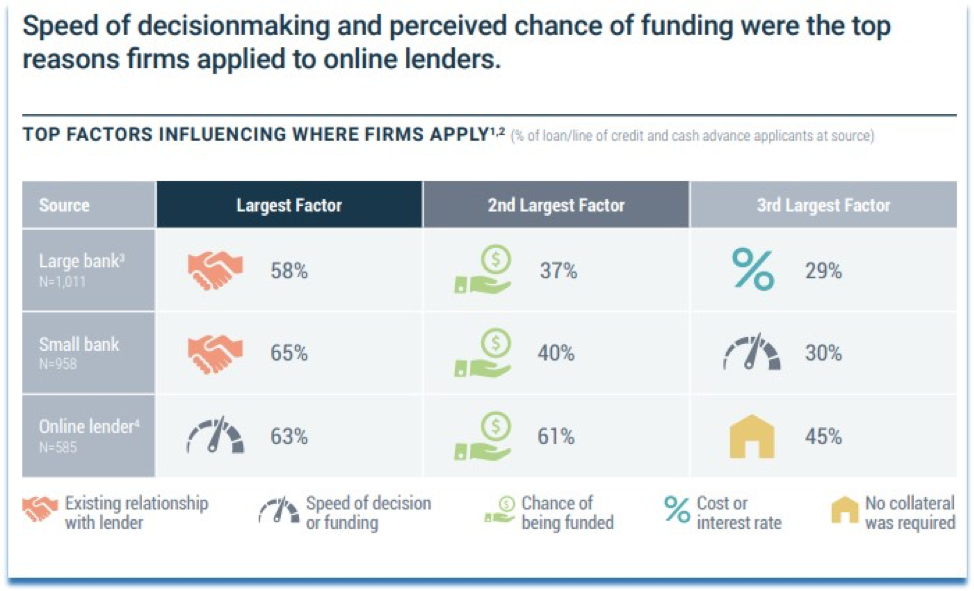

Credit decision speed remains the key driver for this online preference

The New York Fed survey has revealed that the primary benefit business borrowers see with online lenders is the time it takes to render a credit decision. This is followed by the perceived chance of being funded, as online lenders have historically higher approval rates.

Interest rates and loan structure remain the key reasons why banks are still the preferred source for loans and lines of credit

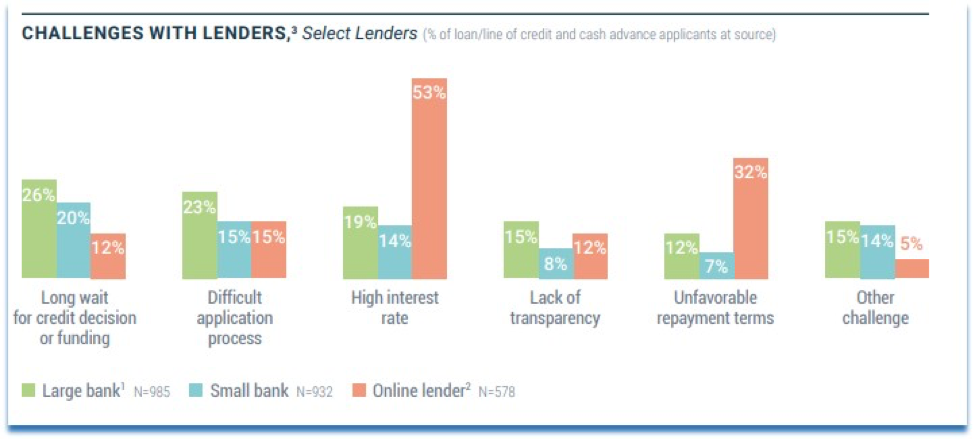

While wait times are the most pervasive complaint borrowers have regarding banks, interest rates and payment terms are the main objection to online lenders. Of course, the rates are dependent on credit quality of the facilities as well as the cost of funds incurred by the online lenders.

We expect that, in the years to come, online lenders will compete more effectively on price, especially for the relationships that offer higher credit quality. While this will depend on their own access to capital, the trend toward the use of more efficient technology is helping to drive down their operating costs.

The next few years are important in determining the path of online lending

The data in these surveys indicates that chartered financial institutions still hold the advantage in attracting business borrowers, but that online lenders continue to gain ground. The best path forward for banks is to take advantage of their strengths while also trying to eliminate these weaknesses. Many financial institutions have gone down this path in recent years by beginning to offer streamlined application processes using both web and mobile technology. Through this path of online loan origination, they have effectively eliminated the reason for credit worthy borrowers to apply with online lenders.

The worst mistake banks could make is ignoring these trends. Remember that we have seen similar trends in the past, related to consumer loans and mortgages. Commercial loans continue to be a significant driver of income for banks of all sizes. Now is the time to protect your turf by offering some of the same streamlined origination options that your competition is using to lure business away from you. If banks can do this while still offering the same level of personalized service they’re known for, their chances of success will be even stronger.

That is the primary opportunity. Lending technology today can seamlessly complement banks’ current underwriting practices and workflows, allowing them to effectively offer the best of both world and better compete.

[“source=bankingexchange”]